Introduction

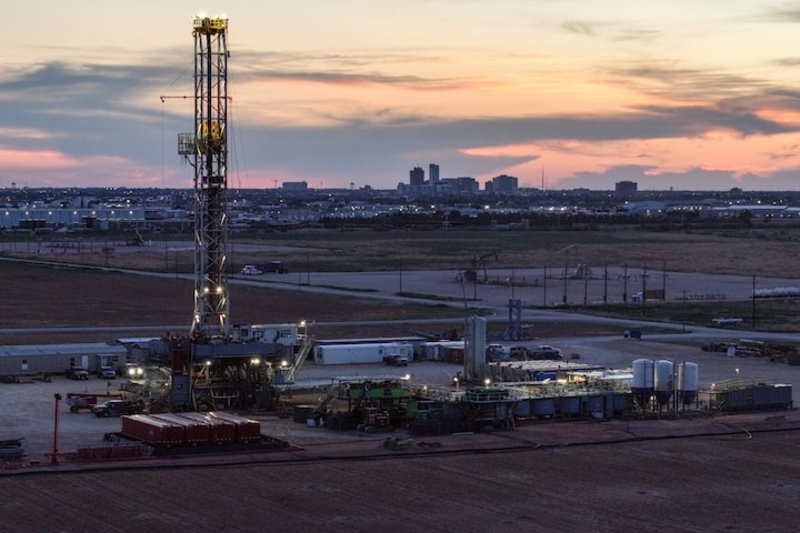

Oil prices faced renewed pressure on Friday after U.S. energy companies reduced the number of active drilling rigs for the first time in six weeks, signaling a potential slowdown in domestic output growth. According to data reported by Reuters, Baker Hughes’ weekly rig count showed a decline of three rigs, bringing the total number of active oil rigs in the United States to 496. The modest but symbolic reduction comes at a time when global markets are already grappling with weakening demand signals and fluctuating dollar strength.

The shift in rig activity highlights how producers are adjusting to a volatile environment shaped by uncertain policy direction, changing capital costs, and a market oversupplied by non-OPEC producers. Although the cut is small, analysts see it as an early indication that drilling momentum may be tapering off after months of expansion. With U.S. production hovering near record highs, even minor reductions in field activity can have ripple effects on market sentiment and forward price expectations.

Drilling Activity and Production Trends

The U.S. shale sector has been one of the dominant forces in global oil supply over the past decade. Output surged as technology and efficiency gains made tight oil production more cost effective. However, in recent months, operators have faced tightening credit conditions, inflation in equipment costs, and mixed price signals. The result has been a cautious approach to new drilling, with producers focusing on maximizing returns from existing wells rather than aggressive expansion.

According to the Baker Hughes data, the most significant rig reductions occurred in the Permian Basin of West Texas and New Mexico, the largest and most productive shale region in the United States. Two rigs were also idled in the Eagle Ford and Williston basins. Despite these declines, overall U.S. crude production remains near 13.3 million barrels per day, close to an all time high. Analysts note that efficiency gains and longer lateral wells mean fewer rigs are needed to sustain high output levels compared to earlier years.

Market Reaction and Price Implications

The immediate market reaction to the rig data was muted, with oil prices falling modestly during afternoon trading. Brent crude futures settled around 81 dollars per barrel, while West Texas Intermediate (WTI) hovered near 76 dollars. Traders said the decline in rig count offered limited support because the overall production outlook remains strong. In addition, rising inventories and soft demand in Asia have continued to weigh on sentiment.

Bloomberg reported that speculative traders reduced net long positions in crude futures for a second consecutive week, reflecting caution about the market’s near term direction. The dollar’s strength has added further pressure by making oil more expensive for holders of other currencies. Analysts from Trading Economics observed that unless demand improves meaningfully in the coming months, production restraint alone may not be sufficient to lift prices significantly.

Capital Discipline and Cost Pressures

One of the defining features of the current U.S. oil market is the emphasis on capital discipline. Publicly listed producers have prioritized shareholder returns through dividends and buybacks instead of reinvesting aggressively in new wells. This conservative strategy reflects lessons learned from the boom and bust cycles of the past decade, where overexpansion often led to financial strain.

Rising costs have also contributed to the slowdown in drilling. Inflation in steel, labor, and equipment has increased the breakeven prices for many producers. Data from the Dallas Federal Reserve’s energy survey shows that the average breakeven cost in the Permian Basin has risen from 48 to 56 dollars per barrel over the past year. For smaller independent drillers, these higher costs, combined with tight financing conditions, make it difficult to sustain previous drilling paces.

Global Context and OPEC+ Strategy

The U.S. slowdown arrives as OPEC and its allies maintain tight control over output levels. OPEC+ has extended its voluntary production cuts through the end of the year, aiming to prevent a price collapse amid fragile demand. Saudi Arabia and Russia have reiterated their commitment to market stability but have expressed concern over the resilience of U.S. shale output.

For much of the past two years, U.S. production growth has offset OPEC+ discipline, limiting the effectiveness of supply management efforts. A sustained reduction in drilling could ease this tension by slowing the rate of U.S. output growth and rebalancing the global market. However, given that many U.S. producers can scale operations quickly, OPEC officials remain cautious about predicting lasting changes.

Dollar Strength and Oil Trade Dynamics

The fluctuating U.S. dollar continues to play a key role in shaping global oil trade. The dollar index has oscillated near 105 in recent weeks, supported by strong U.S. economic data and investor demand for safe haven assets. While this has bolstered U.S. purchasing power, it has also dampened demand in major importing nations such as India and China, where local currencies have weakened.

As oil is priced in dollars, a stronger greenback typically exerts downward pressure on prices by making imports more expensive for other countries. According to Reuters market analysts, this dynamic is contributing to the broader softness in global oil demand, particularly in emerging markets that are sensitive to currency fluctuations. Traders are now watching for upcoming U.S. inflation data and Federal Reserve comments that could determine whether the dollar’s strength persists into year end.

Industry Sentiment and Corporate Guidance

Energy executives have struck a cautious tone in recent earnings calls, emphasizing profitability over production growth. Several major producers, including ExxonMobil and Chevron, have reiterated that future drilling activity will depend on sustained price stability above 75 dollars per barrel. Smaller operators have echoed this sentiment, saying they will prioritize debt reduction and cash flow management in the face of uncertain market conditions.

According to MarketWatch, forward rig bookings for the fourth quarter have declined slightly, suggesting continued moderation in field activity. Drilling contractors report lower demand for short term rig leases, while service providers expect slower growth in equipment utilization. Despite these headwinds, most firms remain profitable, supported by hedging strategies and stable refining margins.

Energy Transition and Policy Influence

The broader energy transition is also shaping decisions within the U.S. oil sector. Federal incentives for renewable energy projects, coupled with stricter emissions regulations, are gradually influencing investment priorities. While oil remains the backbone of U.S. energy production, companies are diversifying portfolios to include natural gas, carbon capture, and low carbon fuels.

This shift, combined with public and investor pressure for sustainability, has led to a more measured approach toward fossil fuel expansion. Analysts at the International Energy Agency note that U.S. producers are increasingly factoring environmental metrics into capital allocation decisions. The slowdown in drilling activity may thus represent not only an economic adjustment but also a structural pivot toward a more balanced energy strategy.

Outlook and Key Indicators

Looking ahead, analysts expect drilling activity to remain steady or decline slightly through the fourth quarter unless prices recover meaningfully. Seasonal maintenance at refineries and weaker demand from Europe could further constrain oil consumption. However, should geopolitical tensions escalate or OPEC+ tighten output more aggressively, the balance could shift again in favor of higher prices.

Investors will monitor weekly rig counts, production estimates, and inventory data for early signs of supply side tightening. The U.S. Energy Information Administration’s next report will provide updated projections on shale output, which could influence price expectations heading into winter.

Conclusion

The first reduction in U.S. drilling rigs in six weeks may appear modest, but it carries symbolic weight in a market searching for equilibrium. With production near record highs, the decline reflects a subtle but meaningful shift toward caution among U.S. producers. Rising costs, financial discipline, and policy uncertainty are converging to slow the expansion that defined much of the post pandemic recovery period.

For global oil markets, the development underscores the fragility of the current balance between supply and demand. If U.S. output begins to flatten while OPEC+ maintains its curbs, the resulting tightening could stabilize prices in the coming months. Yet, as long as the dollar remains strong and demand growth subdued, the path forward for oil will depend less on production capacity and more on economic confidence worldwide.